Spot & forward rates are settlement prices of spot & forward contracts; cross rates are the exchange rate between two unofficial currencies.

Learning Objectives

Differentiate between spot rates, forward rates, and cross rates

Key Takeaways

Key Points

- A spot contract is a contract of buying or selling a commodity, security or currency for settlement (payment and delivery) on the spot date, which is normally two business days after the trade date. The settlement price (or rate) is called spot price or spot rate.

- A spot contract is in contrast with a forward contract where contract terms are agreed now but delivery and payment will occur at a future date. The settlement price of a forward contract is called forward price or forward rate.

- Spot rates can be used to calculate forward rates. In theory, the difference in spot and forward prices should be equal to the finance charges, plus any earnings due to the holder of the security, according to the cost of carry model.

- A cross rate is the currency exchange rate between two currencies, both of which are not the official currencies of the country in which the exchange rate quote is given in.

Key Terms

- bootstrapping method: In finance, bootstrapping is a method for constructing a (zero-coupon) fixed-income yield curve from the prices of a set of coupon-bearing products (e.g., bonds and swaps).Using these zero-coupon products, it becomes possible to derive par swap rates (forward and spot) for all maturities by making a few assumptions (including linear interpolation). The term structure of spot returns is recovered from the bond yields by solving for them recursively, by forward substitution. This iterative process is called the Bootstrap Method.

Spot Rates

In finance, a spot contract, spot transaction, or simply “spot,” is a contract of buying or selling a commodity, security, or currency for settlement (payment and delivery) on the spot date, which is normally two business days after the trade date. The settlement price (or rate) is called a “spot price” or “spot rate. ”

For bonds, spot rates are estimated via the bootstrapping method, which uses prices of the securities currently trading in market, that is, from the cash or coupon curve. The result is the spot curve, which exists for fixed income securities.

Forward Rates

A spot contract is in contrast with a forward contract where contract terms are agreed now but delivery and payment will occur at a future date. The settlement price of a forward contract is called a “forward price” or “forward rate. ” Depending on the item being traded, spot prices can indicate market expectations of future price movements. In other words, spot rates can be used to calculate forward rates. In theory, the difference in spot and forward prices should be equal to the finance charges, plus any earnings due to the holder of the security, according to the cost of carry model. For example, on a share, the difference in price between the spot and forward is usually accounted for almost entirely by any dividends payable in the period minus the interest payable on the purchase price.

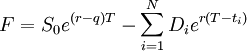

If the underlying asset is tradeable, the forward price is given by:

where F is the forward price to be paid at time, Tex is the exponential function (used for calculating compounding interests), r is the risk-free interest rate, q is the cost-of-carry, S0 is the spot price of the asset (i.e., what it would sell for at time 0), Di is a dividend which is guaranteed to be paid at time ti where 0< ti< T.

Cross Rates

A cross rate is the currency exchange rate between two currencies, both of which are not the official currencies of the country in which the exchange rate quote is given in. This phrase is also sometimes used to refer to currency quotes which do not involve the U.S. dollar, regardless of which country the quote is provided in. For example, if an exchange rate between the euro and the Japanese yen was quoted in an American newspaper, this would be considered a cross rate in this context, because neither the euro or the yen is the standard currency of the U.S. However, if the exchange rate between the euro and the U.S. dollar were quoted in that same newspaper, it would not be considered a cross rate because the quote involves the U.S. official currency.

Licenses and Attributions

CC licensed content, Shared previously

- Curation and Revision. Provided by: Boundless.com. License: CC BY-SA: Attribution-ShareAlike

CC licensed content, Specific attribution

- Forward price. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Spot rate. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- bootstrapping method. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Forward price. Provided by: Wikipedia. License: Public Domain: No Known Copyright