Defining Capital Budgeting

Capital budgeting is the planning process used to determine which of an organization’s long term investments are worth pursuing.

Learning Objectives

Differentiate between the different capital budget methods

Key Takeaways

Key Points

- Capital budgeting, which is also called investment appraisal, is the planning process used to determine whether an organization’s long term investments, major capital, or expenditures are worth pursuing.

- Major methods for capital budgeting include Net present value, Internal rate of return, Payback period, Profitability index, Equivalent annuity and Real options analysis.

- The IRR method will result in the same decision as the NPV method for non- mutually exclusive projects in an unconstrained environment; Nevertheless, for mutually exclusive projects, the decision rule of taking the project with the highest IRR may select a project with a lower NPV.

Key Terms

- APT: In finance, arbitrage pricing theory (APT) is a general theory of asset pricing that holds, which holds that the expected return of a financial asset can be modeled as a linear function of various macro-economic factors or theoretical market indices, where sensitivity to changes in each factor is represented by a factor-specific beta coefficient.

- Modified Internal Rate of Return: The modified internal rate of return (MIRR) is a financial measure of an investment’s attractiveness. It is used in capital budgeting to rank alternative investments of equal size. As the name implies, MIRR is a modification of the internal rate of return (IRR) and, as such, aims to resolve some problems with the IRR.

Capital Budgeting

Capital budgeting, which is also called “investment appraisal,” is the planning process used to determine which of an organization’s long term investments such as new machinery, replacement machinery, new plants, new products, and research development projects are worth pursuing. It is to budget for major capital investments or expenditures.

Major Methods

Many formal methods are used in capital budgeting, including the techniques as followed:

- Net present value

- Internal rate of return

- Payback period

- Profitability index

- Equivalent annuity

- Real options analysis

Net Present Value

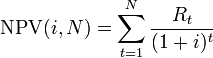

Net present value (NPV) is used to estimate each potential project’s value by using a discounted cash flow (DCF) valuation. This valuation requires estimating the size and timing of all the incremental cash flows from the project. The NPV is greatly affected by the discount rate, so selecting the proper rate–sometimes called the hurdle rate–is critical to making the right decision.

This should reflect the riskiness of the investment, typically measured by the volatility of cash flows, and must take into account the financing mix. Managers may use models, such as the CAPM or the APT, to estimate a discount rate appropriate for each particular project, and use the weighted average cost of capital(WACC) to reflect the financing mix selected. A common practice in choosing a discount rate for a project is to apply a WACC that applies to the entire firm, but a higher discount rate may be more appropriate when a project’s risk is higher than the risk of the firm as a whole.

Internal Rate of Return

The internal rate of return (IRR) is defined as the discount rate that gives a net present value (NPV) of zero. It is a commonly used measure of investment efficiency.

The IRR method will result in the same decision as the NPV method for non-mutually exclusive projects in an unconstrained environment, in the usual cases where a negative cash flow occurs at the start of the project, followed by all positive cash flows. Nevertheless, for mutually exclusive projects, the decision rule of taking the project with the highest IRR, which is often used, may select a project with a lower NPV.

One shortcoming of the IRR method is that it is commonly misunderstood to convey the actual annual profitability of an investment. Accordingly, a measure called “Modified Internal Rate of Return (MIRR)” is often used.

Payback Period

Payback period in capital budgeting refers to the period of time required for the return on an investment to “repay” the sum of the original investment. Payback period intuitively measures how long something takes to “pay for itself. ” All else being equal, shorter payback periods are preferable to longer payback periods.

The payback period is considered a method of analysis with serious limitations and qualifications for its use, because it does not account for the time value of money, risk, financing, or other important considerations, such as the opportunity cost.

Profitability Index

Profitability index (PI), also known as profit investment ratio (PIR) and value investment ratio (VIR), is the ratio of payoff to investment of a proposed project. It is a useful tool for ranking projects, because it allows you to quantify the amount of value created per unit of investment.

Equivalent Annuity

The equivalent annuity method expresses the NPV as an annualized cash flow by dividing it by the present value of the annuity factor. It is often used when comparing investment projects of unequal lifespans. For example, if project A has an expected lifetime of seven years, and project B has an expected lifetime of 11 years, it would be improper to simply compare the net present values (NPVs) of the two projects, unless the projects could not be repeated.

Real Options Analysis

The discounted cash flow methods essentially value projects as if they were risky bonds, with the promised cash flows known. But managers will have many choices of how to increase future cash inflows or to decrease future cash outflows. In other words, managers get to manage the projects, not simply accept or reject them. Real options analysis try to value the choices–the option value–that the managers will have in the future and adds these values to the NPV.

These methods use the incremental cash flows from each potential investment or project. Techniques based on accounting earnings and accounting rules are sometimes used. Simplified and hybrid methods are used as well, such as payback period and discounted payback period.

The Goals of Capital Budgeting

The main goals of capital budgeting are not only to control resources and provide visibility, but also to rank projects and raise funds.

Learning Objectives

Describe the goals of the capital budgeting process

Key Takeaways

Key Points

- Basically, the purpose of budgeting is to provide a forecast of revenues and expenditures and construct a model of how business might perform financially.

- Capital Budgeting is most involved in ranking projects and raising funds when long-term investment is taken into account.

- Capital budgeting is an important task as large sums of money are involved and a long-term investment, once made, can not be reversed without significant loss of invested capital.

Key Terms

- Common stock: Common stock is a form of corporate equity ownership, a type of security.

- Preferred Stock: Preferred stock (also called preferred shares, preference shares or simply preferreds) is an equity security with properties of both an equity and a debt instrument, and is generally considered a hybrid instrument.

The purpose of budgeting is to provide a forecast of revenues and expenditures. That is, to construct a model of how a business might perform financially if certain strategies, events, and plans are carried out. It enables the actual financial operation of the business to be measured against the forecast, and it establishes the cost constraint for a project, program, or operation.

Budgeting helps to aid the planning of actual operations by forcing managers to consider how the conditions might change, and what steps should be taken in such an event. It encourages managers to consider problems before they arise. It also helps co-ordinate the activities of the organization by compelling managers to examine relationships between their own operation and those of other departments.

Other essential functions of a budget include:

- To control resources

- To communicate plans to various responsibility center managers

- To motivate managers to strive to achieve budget goals

- To evaluate the performance of managers

- To provide visibility into the company’s performance

Capital Budgeting, as a part of budgeting, more specifically focuses on long-term investment, major capital and capital expenditures. The main goals of capital budgeting involve:

Ranking Projects

The real value of capital budgeting is to rank projects. Most organizations have many projects that could potentially be financially rewarding. Once it has been determined that a particular project has exceeded its hurdle, then it should be ranked against peer projects (e.g. – highest Profitability index to lowest Profitability index). The highest ranking projects should be implemented until the budgeted capital has been expended.

Raising funds

When a corporation determines its capital budget, it must acquire funds. Three methods are generally available to publicly-traded corporations: corporate bonds, preferred stock, and common stock. The ideal mix of those funding sources is determined by the financial managers of the firm and is related to the amount of financial risk that the corporation is willing to undertake.

Corporate bonds entail the lowest financial risk and, therefore, generally have the lowest interest rate. Preferred stock have no financial risk but dividends, including all in arrears, must be paid to the preferred stockholders before any cash disbursements can be made to common stockholders; they generally have interest rates higher than those of corporate bonds. Finally, common stocks entail no financial risk but are the most expensive way to finance capital projects.The Internal Rate of Return is very important.

Capital budgeting is an important task as large sums of money are involved, which influences the profitability of the firm. Plus, a long-term investment, once made, cannot be reversed without significant loss of invested capital. The implication of long-term investment decisions are more extensive than those of short-run decisions because of the time factor involved; capital budgeting decisions are subject to a higher degree of risk and uncertainty than are short-run decisions.

Accounting Flows and Cash Flows

Capital budgeting requires a thorough understanding of cash flow and accounting principles, particularly as they pertain to valuing processes and investments.

Learning Objectives

Identify the various sources of cash flow within an organization

Key Takeaways

Key Points

- Accounting revolves around tracking the inflows and outflows of assets, capital, and resources for an organization to adhere to legal and investor expectations.

- When measuring the impact of assets, liabilities, and equity, it is useful to know in which situations to debit or credit the line item based upon the flow of capital.

- Cash flows analyses, such as the internal rate of return (IRR) or the net present value (NPV) of a given process, are core tools in capital budgeting for understanding and estimating cash flows.

- Cash flow analyses can include investing, operating and financing activities.

Key Terms

- net present value (NPV): This calculation takes all future cash flows from a given operational initiative, and discounts them to their present value based on the weighted average cost of capital.

- internal rate of return (IRR): A calculation that makes the net present value of all cash flows (positive and negative) from a particular investment equal to zero. It can also be described as the rate which will make an investment break even.

Accounting Flows

Accounting is the processes used to identify and transpose business transactions into permanent legal records of a business’s operations and capital flows. The International Accounting Standards (IAS) and the Generally Accepted Accounting Principles (GAAP) are legislative descriptions of expectations and norms within the accounting field.

When it comes to the capital flows in accounting, it is easiest to visualize it based on each type of item:

Understanding how to report each type of asset, and the impacts these asset changes have on income statements, balance sheets, and cash flow statements, is important in accurately depicting accounting flows.

Cash Flows

A cash flow is one element of accounting flows, and particularly important to understanding capital budgeting. A cash flow describes the transmission of payments and returns internally and/or externally as a byproduct of operations over time. Conducting cash flow analyses on current or potential projects and investments is a critical aspect of capital budgeting, and determines the profitability, cost of capital, and/or expected rate of return on a given project, organizational operation or investment.

Cash flow analyses can reveal the rate of return, or value of suggested project, through deriving the internal rate of return (IRR) and the net present value (NPV). They also indicate overall liquidity, or a business’s capacity to capture existing opportunities through freeing of capital for future investments. Cash flows will also underline overall profitability including, but not limited to, net income.

Cash flows consolidate inputs from the following activities:

- Investing activities – Payments related to mergers or acquisitions, loans made to suppliers or received from customers, as well as the purchase or sale of assets are all considered investing activities and tracked as incoming or outgoing cash flows.

- Operating activities – Operating activities can be quite broad, incorporating anything related to the production, sale, or delivery of a given product or service. This includes raw materials, advertising, shipping, inventory, payments to suppliers and employee, interest payments, depreciation, deferred tax, and amortization.

- Financing activities – Financing activities primarily revolve around cash inflows from banks and shareholders, as well as outflows via dividends to investors. This includes, payment for repurchase of company shares, dividends, net borrowing and net repayment of debt.

Ranking Investment Proposals

Several methods are commonly used to rank investment proposals, including NPV, IRR, PI, payback period, and ARR.

Learning Objectives

Analyze investment proposals by ranking them using different methods

Key Takeaways

Key Points

- The higher the NPV, the more attractive the investment proposal.

- The higher a project’s IRR, the more desirable it is to undertake the project.

- As the value of the profitability index increases, so does the financial attractiveness of the proposed project.

- Shorter payback periods are preferable to longer payback periods.

- The higher the ARR, the more attractive the investment.

Key Terms

- discounted cash flow: In finance, discounted cash flow (DCF) analysis is a method of valuing a project, company, or asset using the concepts of the time value of money.

- time value of money: The time value of money is the value of money, figuring in a given amount of interest earned over a given amount of time.

The most valuable aim of capital budgeting is to rank investment proposals. To choose the most valuable investment option, several methods are commonly used:

Net Present Value (NPV):

NPV can be described as the “difference amount” between the sums of discounted: cash inflows and cash outflows. In the case when all future cash flows are incoming, and the only outflow of cash is the purchase price, the NPV is simply the PV of future cash flows minus the purchase price (which is its own PV). The higher the NPV, the more attractive the investment proposal. NPV is a central tool in discounted cash flow (DCF) analysis and is a standard method for using the time value of money to appraise long-term projects. Used for capital budgeting and widely used throughout economics, finance, and accounting, it measures the excess or shortfall of cash flows, in present value terms, once financing charges are met.

In financial theory, if there is a choice between two mutually exclusive alternatives, the one yielding the higher NPV should be selected. The rules of decision making are:

- When NPV > 0, the investment would add value to the firm so the project may be accepted

- When NPV < 0, the investment would subtract value from the firm so the project should be rejected

- When NPV = 0, the investment would neither gain nor lose value for the firm. We should be indifferent in the decision whether to accept or reject the project. This project adds no monetary value. Decision should be based on other criteria (e.g., strategic positioning or other factors not explicitly included in the calculation).

An NPV calculated using variable discount rates (if they are known for the duration of the investment) better reflects the situation than one calculated from a constant discount rate for the entire investment duration.

Internal Rate of Return (IRR)

The internal rate of return on an investment or project is the “annualized effective compounded return rate” or “rate of return” that makes the net present value (NPV as NET*1/(1+IRR)^year) of all cash flows (both positive and negative) from a particular investment equal to zero.

IRR calculations are commonly used to evaluate the desirability of investments or projects. The higher a project’s IRR, the more desirable it is to undertake the project. Assuming all projects require the same amount of up-front investment, the project with the highest IRR would be considered the best and undertaken first.

Profitability Index (PI)

It is a useful tool for ranking projects, because it allows you to quantify the amount of value created per unit of investment. The ratio is calculated as follows:

Profitability index = PV of future cash flows / Initial investment

As the value of the profitability index increases, so does the financial attractiveness of the proposed project. Rules for selection or rejection of a project:

- If PI > 1 then accept the project

- If PI < 1 then reject the project

Payback Period

Payback period intuitively measures how long something takes to “pay for itself. ” All else being equal, shorter payback periods are preferable to longer payback periods. Payback period is widely used because of its ease of use despite the recognized limitations: The time value of money is not taken into account.

Accounting Rate of Return (ARR)

The ratio does not take into account the concept of time value of money. ARR calculates the return, generated from net income of the proposed capital investment. The ARR is a percentage return. Say, if ARR = 7%, then it means that the project is expected to earn seven cents out of each dollar invested. If the ARR is equal to or greater than the required rate of return, the project is acceptable. If it is less than the desired rate, it should be rejected. When comparing investments, the higher the ARR, the more attractive the investment. Basic formulae:

ARR = Average profit / Average investment

Where: Average investment = (Book value at beginning of year 1 + Book value at end of user life) / 2

Reinvestment Assumptions

NPV and PI assume reinvestment at the discount rate, while IRR assumes reinvestment at the internal rate of return.

Learning Objectives

Identify the reinvestment assumptions of different capital budgeting methods

Key Takeaways

Key Points

- If trying to decide between alternative investments in order to maximize the value of the firm, the reinvestment rate would be a better choice.

- NPV and PI assume reinvestment at the discount rate.

- IRR assumes reinvestment at the internal rate of return.

Key Terms

- Weighted average cost of capital: The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets.

Reinvestment Rate

To some extent, the selection of the discount rate is dependent on the use to which it will be put. If the intent is simply to determine whether a project will add value to the company, using the firm’s weighted average cost of capital may be appropriate. If trying to decide between alternative investments in order to maximize the value of the firm, the corporate reinvestment rate would probably be a better choice.

NPV Reinvestment Assumption

The rate used to discount future cash flows to the present value is a key variable of this process. A firm’s weighted average cost of capital (after tax) is often used, but many people believe that it is appropriate to use higher discount rates to adjust for risk or other factors. A variable discount rate with higher rates applied to cash flows occurring further along the time span might be used to reflect the yield curve premium for long-term debt.

Another approach to choosing the discount rate factor is to decide the rate that the capital needed for the project could return if invested in an alternative venture. Related to this concept is to use the firm’s reinvestment rate. Reinvestment rate can be defined as the rate of return for the firm’s investments on average. When analyzing projects in a capital constrained environment, it may be appropriate to use the reinvestment rate, rather than the firm’s weighted average cost of capital as the discount factor. It reflects opportunity cost of investment, rather than the possibly lower cost of capital.

PI Reinvestment Assumption

Profitability index assumes that the cash flow calculated does not include the investment made in the project, which means PI reinvestment at the discount rate as NPV method. A profitability index of 1 indicates break even. Any value lower than one would indicate that the project’s PV is less than the initial investment. As the value of the profitability index increases, so does the financial attractiveness of the proposed project.

IRR Reinvestment Assumption

As an investment decision tool, the calculated IRR should not be used to rate mutually exclusive projects but only to decide whether a single project is worth the investment. In cases where one project has a higher initial investment than a second mutually exclusive project, the first project may have a lower IRR (expected return) but a higher NPV (increase in shareholders ‘ wealth) and, thus, should be accepted over the second project (assuming no capital constraints).

IRR assumes reinvestment of interim cash flows in projects with equal rates of return (the reinvestment can be the same project or a different project). Therefore, IRR overstates the annual equivalent rate of return for a project that has interim cash flows which are reinvested at a rate lower than the calculated IRR. This presents a problem, especially for high IRR projects, since there is frequently not another project available in the interim that can earn the same rate of return as the first project.

When the calculated IRR is higher than the true reinvestment rate for interim cash flows, the measure will overestimate–sometimes very significantly–the annual equivalent return from the project. This makes IRR a suitable (and popular) choice for analyzing venture capital and other private equity investments, as these strategies usually require several cash investments throughout the project, but only see one cash outflow at the end of the project (e.g., via IPO or M&A).

When a project has multiple IRRs, it may be more convenient to compute the IRR of the project with the benefits reinvested. Accordingly, MIRR is used, which has an assumed reinvestment rate, usually equal to the project’s cost of capital.

Long-Term vs. Short-Term Financing

Long-term financing is generally for assets and projects and short term financing is typically for continuing operations.

Learning Objectives

Classify the different financing methods between short-term and long-term

Key Takeaways

Key Points

- Management must match long-term financing or short-term financing mix to the assets being financed in terms of both timing and cash flow.

- Long-term financing includes equity issued, Corporate bond, Capital notes and so on.

- Short-term financing includes Commercial papers, Promissory notes, Asset-based loans, Repurchase agreements, letters of credit and so on.

Key Terms

- accounts receivable: Accounts receivable also known as Debtors, is money owed to a business by its clients (customers) and shown on its balance sheet as an asset.

- Call option: A call option, often simply labeled a “call”, is a financial contract between two parties, the buyer and the seller of this type of option. [1] The buyer of the call option has the right, but not the obligation to buy an agreed quantity of a particular commodity or financial instrument (the underlying) from the seller of the option at a certain time (the expiration date) for a certain price (the strike price)

- Swap: In finance, a swap is a derivative in which counterparties exchange cash flows of one party’s financial instrument for those of the other party’s financial instrument.

Achieving the goals of corporate finance requires appropriate financing of any corporate investment. The sources of financing are, generically, capital that is self-generated by the firm and capital from external funders, obtained by issuing new debt and equity.

Management must attempt to match the long-term or short-term financing mix to the assets being financed as closely as possible, in terms of both timing and cash flows.

Long-Term Financing

Businesses need long-term financing for acquiring new equipment, R&D, cash flow enhancement and company expansion. Major methods for long-term financing are as follows:

Equity Financing

This includes preferred stocks and common stocks and is less risky with respect to cash flow commitments. However, it does result in a dilution of share ownership, control and earnings. The cost of equity is also typically higher than the cost of debt – which is, additionally, a deductible expense – and so equity financing may result in an increased hurdle rate which may offset any reduction in cash flow risk.

Corporate Bond

A corporate bond is a bond issued by a corporation to raise money effectively so as to expand its business. The term is usually applied to longer-term debt instruments, generally with a maturity date falling at least a year after their issue date.

Some corporate bonds have an embedded call option that allows the issuer to redeem the debt before its maturity date. Other bonds, known as convertible bonds, allow investors to convert the bond into equity.

Capital Notes

Capital notes are a form of convertible security exercisable into shares. They are equity vehicles. Capital notes are similar to warrants, except that they often do not have an expiration date or an exercise price (hence, the entire consideration the company expects to receive, for its future issue of shares, is paid when the capital note is issued). Many times, capital notes are issued in connection with a debt-for-equity swap restructuring: instead of issuing the shares (that replace debt) in the present, the company gives creditors convertible securities – capital notes – so the dilution will occur later.

Short-Term Financing

Short-term financing can be used over a period of up to a year to help corporations increase inventory orders, payrolls and daily supplies. Short-term financing includes the following financial instruments:

Commercial Paper

This is an unsecured promissory note with a fixed maturity of 1 to 364 days in the global money market. It is issued by large corporations to get financing to meet short-term debt obligations. It is only backed by an issuing bank or corporation’s promise to pay the face amount on the maturity date specified on the note. Since it is not backed by collateral, only firms with excellent credit ratings from a recognized rating agency will be able to sell their commercial paper at a reasonable price.

Asset-backed commercial paper (ABCP) is a form of commercial paper that is collateralized by other financial assets. ABCP is typically a short-term instrument that matures between 1 and 180 days from issuance and is typically issued by a bank or other financial institution.

Promissory Note

This is a negotiable instrument, wherein one party (the maker or issuer) makes an unconditional promise in writing to pay a determinate sum of money to the other (the payee), either at a fixed or determinable future time or on demand of the payee, under specific terms.

Asset-based Loan

This type of loan, often short term, is secured by a company’s assets. Real estate, accounts receivable (A/R), inventory and equipment are typical assets used to back the loan. The loan may be backed by a single category of assets or a combination of assets (for instance, a combination of A/R and equipment).

Repurchase Agreements

These are short-term loans (normally for less than two weeks and frequently for just one day) arranged by selling securities to an investor with an agreement to repurchase them at a fixed price on a fixed date.

Letter of Credit

This is a document that a financial institution or similar party issues to a seller of goods or services which provides that the issuer will pay the seller for goods or services the seller delivers to a third-party buyer. The issuer then seeks reimbursement from the buyer or from the buyer’s bank. The document serves essentially as a guarantee to the seller that it will be paid by the issuer of the letter of credit, regardless of whether the buyer ultimately fails to pay.

Licenses and Attributions

CC licensed content, Shared previously

- Curation and Revision. Provided by: Boundless.com. License: CC BY-SA: Attribution-ShareAlike

CC licensed content, Specific attribution

- Capital budgeting. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Payback period. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Profitability index. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Payback period. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- APT. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Modified Internal Rate of Return. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Common stock. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Budget. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Capital budgeting. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Preferred Stock. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- NBGI Private Equity logo. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Budget ESA 2010. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Internal rate of return. Provided by: Wikipedia. Located at: https://en.wikipedia.org/wiki/Internal_rate_of_return. License: CC BY-SA: Attribution-ShareAlike

- Cash flow. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Cash flow statement. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Financial accounting. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Cash flow forecasting. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- NBGI Private Equity logo. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Budget ESA 2010. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Accounting Flows.JPG. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Payback period. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- discounted cash flow. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Internal rate of return. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Accounting rate of return. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Net present value. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Profitability index. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Net present value. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- time value of money. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- NBGI Private Equity logo. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Budget ESA 2010. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Accounting Flows.JPG. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Flickr. License: CC BY: Attribution

- Net present value. Provided by: Wikipedia. License: Public Domain: No Known Copyright

- Net present value. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Profitability index. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Dividend reinvestment plan. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Rate of return. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Internal rate of return. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Weighted average cost of capital. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- NBGI Private Equity logo. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Budget ESA 2010. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Accounting Flows.JPG. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Flickr. License: CC BY: Attribution

- Net present value. Provided by: Wikipedia. License: Public Domain: No Known Copyright

- All sizes | 100416-A8647R-001 | Flickr – Photo Sharing!. Provided by: Flickr. Located at: https://www.flickr.com/photos/armyengineersnorfolk/4535262178/sizes/o/in/photostream/. License: CC BY: Attribution

- Modified internal rate of return. Provided by: Wikipedia. Located at: https://en.wikipedia.org/wiki/Modified_internal_rate_of_return. License: Public Domain: No Known Copyright

- Rate of return. Provided by: Wikipedia. License: Public Domain: No Known Copyright

- Swap. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Capital note. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Commercial paper. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Corporate finance. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Asset-backed commercial paper. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Promissory note. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Asset-based loan. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Corporate bond. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Letter of credit. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Money market. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Call option. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- accounts receivable. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- NBGI Private Equity logo. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Budget ESA 2010. Provided by: Wikimedia. License: Public Domain: No Known Copyright

- Accounting Flows.JPG. Provided by: Wikipedia. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Flickr. License: CC BY: Attribution

- Net present value. Provided by: Wikipedia. License: Public Domain: No Known Copyright

- All sizes | 100416-A8647R-001 | Flickr – Photo Sharing!. Provided by: Flickr. Located at: https://www.flickr.com/photos/armyengineersnorfolk/4535262178/sizes/o/in/photostream/. License: CC BY: Attribution

- Modified internal rate of return. Provided by: Wikipedia. License: Public Domain: No Known Copyright

- Rate of return. Provided by: Wikipedia. License: Public Domain: No Known Copyright

- Financing – Search for Photos. Provided by: Fotopedia. Located at: https://fotopedia.com/search?q=Financing&human_license=reuse_commercial_modify. License: CC BY: Attribution