Learning Objectives

- Explain how sales are the main driver for a financial forecast.

- Determine a past time period to formulate the basis for a financial forecast.

- Explain the advantages and disadvantages of using past data to forecast future financial performance.

- Calculate past sales growth averages.

- Justify adjusting relationships when forecasting future financial performance.

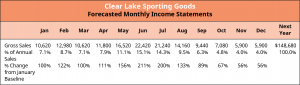

In this section of the chapter, you will begin to explore the first step of creating a forecast: forecasting sales. We will discuss common time frames for sales forecasts and why we use historical data in our forecasts (but only with caution), and we will work through the process of forecasting future sales. We will be using the percent-of-sales method to forecast some expenses for Clear Lake Sporting Goods, the example used throughout the chapter. This method relies on sales data, further highlighting why accuracy in forecasting sales is crucial.

Sales as the Driver

A significant portion of a business’s costs are driven by how much it sells. Thus, the sales forecast is the necessary first step in preparing a financial forecast. Common costs driven by sales include direct product costs, direct labor costs, and other key variable costs (i.e., costs that vary proportionately to sales), such as sales commissions.

Looking to the Past

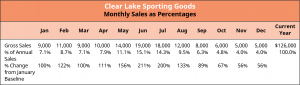

Forecasting sales is not always an easy task, as no one knows the future. We can, however, use the information we do have to forecast future sales with the greatest accuracy possible. Most firms start by looking at the past. A firm may look at past sales from a variety of prior periods. It’s common to look at the past 12 months to estimate the coming 12 months. Looking at 12 consecutive months helps identify seasonality of sales trends, what time of year sales tend to drop off and when they increase, possible sales spikes that might reoccur, and any other trends that tend to appear over a 12-month period. In Figure 18.7, we see Clear Lake’s sales by month for the past 12 months.

Past data is often used in conjunction with probabilities and weighted average calculations derived from probabilities. Though used in several areas of forecasting, this approach is particularly common in drafting the sales forecast. Using multiple scenarios and the probability of each scenario occurring is a common approach to estimating future sales.

This knowledge is helpful when assembling a first pass at the next year’s sales forecast. Using common-size and horizontal (trend) analyses on sales is also helpful, as shown in Figure 18.8. We can see the exact percentages that sales went up or down each month:

- In January, the company had sales of $9,000, which was 7.1%($9.000/$126,000) of the total annual sales.

- In June, the company had $19,000 sales, which was 15.1($19,000/$126,000)

of the total annual sales and 211%($19,000/$9,000) of January sales.